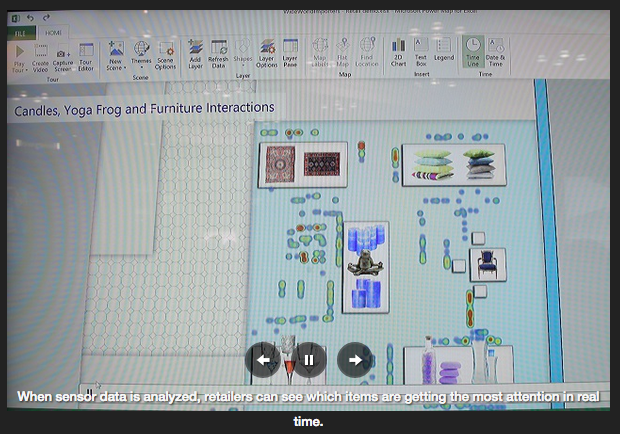

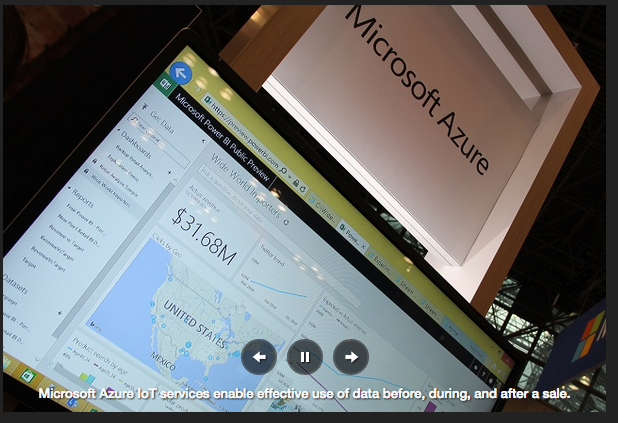

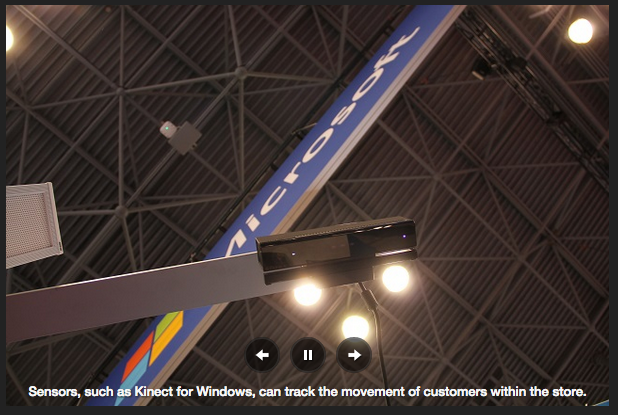

2015 NRF Big Show Recap

Though the full vision of an omnichannel store is still aspirational, investments by retailers and vendors are bringing that vision closer to reality than ever before. This new paradigm in retail --a real-time, data driven, customer-focused, destination-creating, renaissance-- is evolving. I guess that means next year I can go back to New York? Hope so!

Frankly The Best "Ephemeral" Messenger

Models were even available for live chat!

Looking Forward to 2015: Part Two

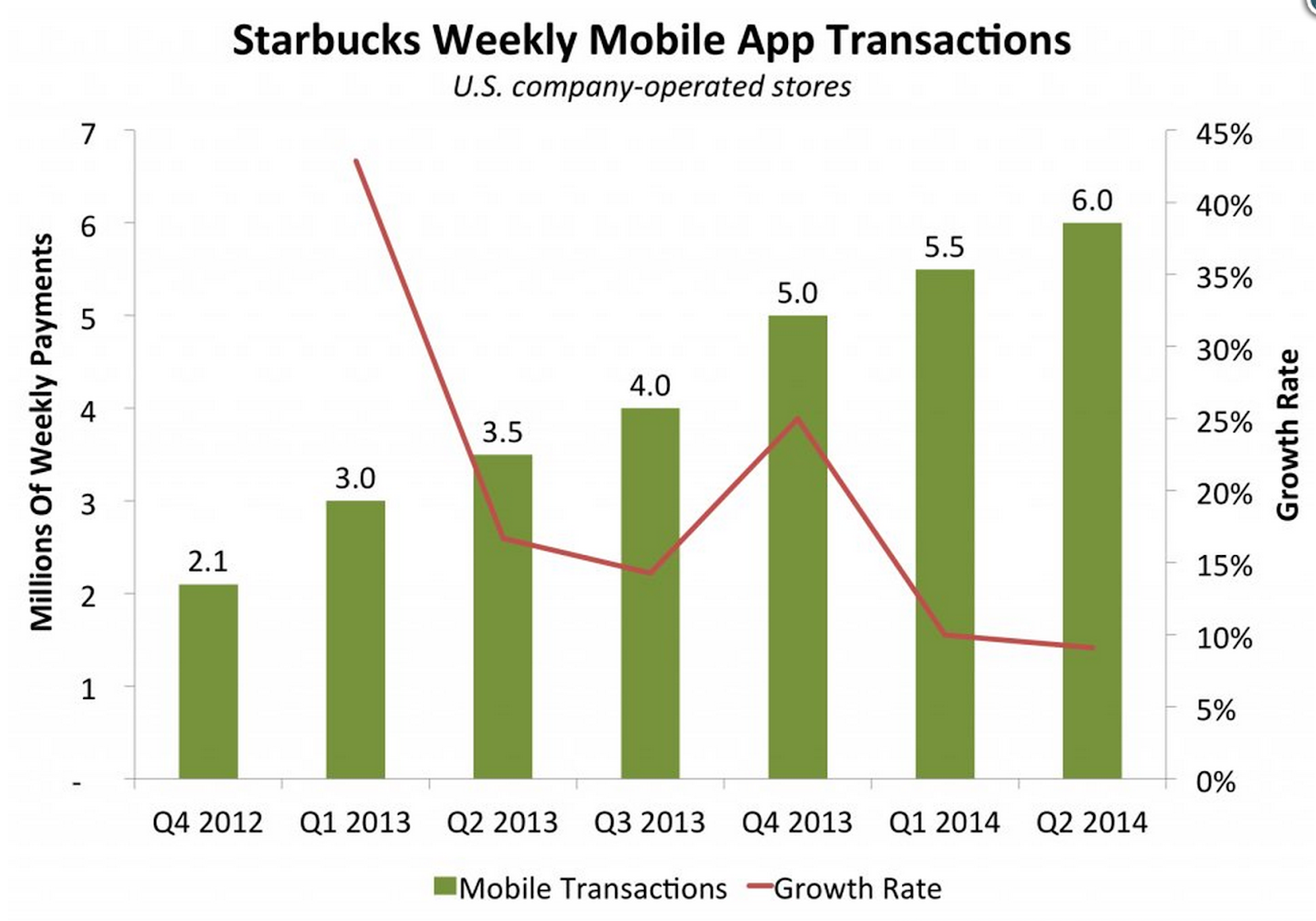

Mobile payments got a huge injection of consumer confidence from the release of Apple Pay. Anyone would assume Apple’s share of global mobile payment transactions will be significant, eventually. But remember, there are several very real competitors. Just a few years ago many predicted that PayPal would “win” the mobile payments market, now Apple Pay is all the rage. The reality is there probably will not be any clear winners, not for a while anyway.

And in fact Apple Pay is not garnering the kind of adoption many had hoped for. Some reports show 1% of transaction volume on mobile can be attributed to Apple Pay, not bad I guess but nothing to really brag about. One report also showed that less than 5% of iPhone owners who could enable Apple Pay had done so, and among them on 30% had used it. That said, Wholefoods (one of the most popular merchants for Apple Pay) claims they are witnessing “significant growth” in usage. So there is a ways to go for Apple yet, but integration of BLE and facial recognition software not to mention the Apple Watch will all drive further use of this payment method.

- Happy, because people with Samsung phones will start using mobile payments too!

- Frustrated, because they’ve had NFC mobile payments for years and nobody cared.

- Worried, because this means Apple will sell more phones.

Paypal and eBay split just weeks after the launch of Apple Pay. It’s unclear that Apple had anything to do with that, but it is telling. Paypal was once considered the front-runner, now they are just one in a peloton where Apple appears to be slightly ahead.

Well, ISIS is a household name but that’s not exactly what At&t had in mind.

Looking Forward to 2015: Part One

Jamming with Storybots!

If you have a young child and an iPad, you need to get into Storybots. Their learning apps are affordable and the videos on Youtube are free… check it out!

Ditching Our Wallets for Mobile

Personally, once a mobile wallet app is ready which truly makes my credit cards go away, my wallet is going in the trash. We are getting closer every day to when we only need our phones, and I can’t wait. It’s so close that the last time I went to the airport I consciously decided not to buy a wallet, because I knew it would be outdated soon.

Amazon's future could be acquisition...

Well, it's a gloomy Monday but don't let the weather keep you down. It just means some makeoli and Korean seafood pancakes are waiting for you somewhere. ;-)

Last week most of us witnessed Amazon's unveiling of the new Prime Delivery drones. Bezos says the service will be running in 4-5 years, despite the challenges and many skeptic reviewers it is entirely possible that will happen. The doubters claim three major issues: vandalism, safety, and theft.

The real BIG THREE challenges have nothing to do with these challenges (which anyone with a mild imagination can figure out how to solve). Rolling out a drone delivery network takes... well, first a (1) NETWORK! Creating any kind of network, software or hardware, is not small task and requires lot's of really smart and creative folks from all levels of abstraction to get down. The next REALLY BIG challenge is the (2) OS. What will run these systems? Android? Not likely. Which leads me to the FINAL BIG challenge, the (3) battery. Even if you manage to get the right network, and the right OS... you still need a battery -- of course, if you read my email about Graphene you might not consider this to great a challenge!

Enter... the entrepreneur.

Matternet is an awesome startup that will be either the next big platform or, at the very least, a significant acquisition down the road. Backed by Andreesen Horowitz (two guys who have a knack for early-stage investing I'd say) the company is rolling out it's network where the walled gardens have the North can happily get involved... Africa. How do you convince an unwilling populace to adopt the technology? Make it about helping people (since it is ultimately anyway!). How do you get your medicine in 30min instead of 5 days? Drones.

The company was founded way back in 2011, and has since developed it's first drone which can carry a small package. Their ultimate goal is to deploy delivery drones which can carry up to 1000kg.

Enjoy... and BTW if you're from Seoul watch the video for a neat surprise.

https://mttr.net

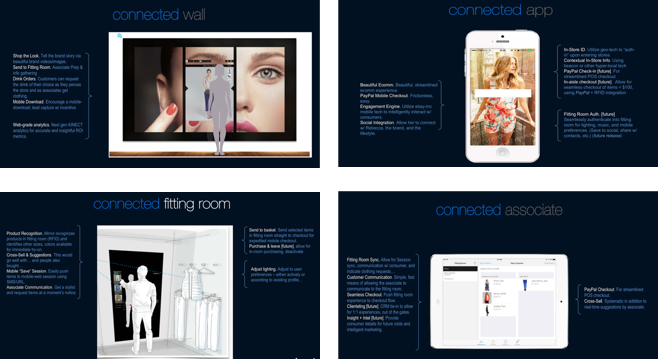

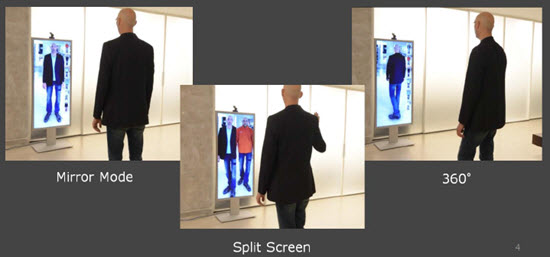

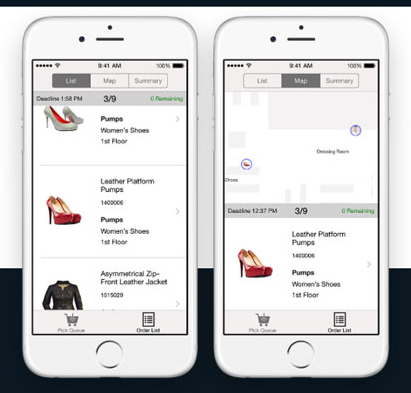

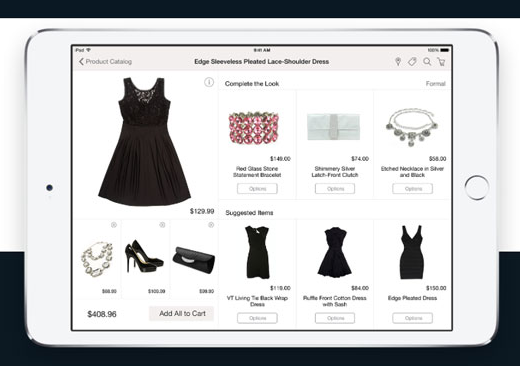

Bio-hacking, the end of Jolt, and the future of retail

Investing In Education

Content Is King

Content Marketing is not new, but it has changed dramatically in the past 10 years or so. Mashable released a simple yet effective illustration a while back, which I came across while looking through my old bookmarks. They described this shift as a comparison between “Content That Humans What to Share” vs. “Content That Ranks High in Search.” While there was a noticeable disconnect in 2002, by 2012 content people wanted to share and high search ranks were in near alignment.

That article was about SEO, Search Engine Optimization, and included some wise-words from SEO Moz CEO Rand Fishkin about what kind of content businesses or start-ups should create to get noticed in this “new” paradigm. The conclusion... basically, “good.”

It’s impossible to say at a granular-level what “good content” is. We can all only speculate and abide by some fairly good guiding points:

1. Good content must be genuine.

Naturally, I intend to tap-away on my keyboard for the next 20 minutes or so to provide some thoughtful ideas about each of these points. But first, it’s important to consider just how important content is for business. 86% of B2C marketers use content marketing, and are spending 28% of their marketing budget on that content (37% for companies with less than 10 employees!). And that budget is enormous, reaching $100 Billion in 2012 and estimated to increase to nearly $120 Billion in 2013.

1. Good Content Must Be Genuine

There are lot’s of ways to interpret this, so here’s what I mean. You want to genuinely want to improve your consumers experience, life, cup-of-coffee. Whatever it is you are into, you are into it because you sincerely see a way you can help improve the community. Think about it.

Ultimately, your business (user-base, etc) will grow because influential people like what you are doing. This doesn’t have to be some cohort of celebrities, but ultimately it may be. People will want to work with you, will want to support you, if they feel you are doing something they believe in. In the words of Simon Sinek, author of Start With Why, “people don’t buy what you do, they buy why you do it.”

2. Good Content Tells A Compelling Story About Your Brand

This is not the same as point 1, but yeah they are (they all are) related. YOU MUST HAVE A STORY... this doesn’t matter if you are selling yourself, selling your business, or selling a house. Stories sell, and for lot’s of good reasons.

Your story is what is going to convey that genuine desire, it’s the vehicle that carries your excitement, your inspiration, your love, your frustration, whatever emotions you feel are motivating you to do whatever it is you are doing... those are carried to the hearts and minds of your audience via the words, those compelling words of your story.

You can start getting the right story by having the right mission statement. Your mission statement should convey your reason for existence, your "why," in addition to some hint at "what" you do.

It’s like the mantra of your brand. Make sure you nail it! Check this out.